VAT

Bill (V-bill) The Writer's website

[Original draft created by Lal Silva (Deputy

Commissioner General, Inland Revenue Sri Lanka) on 25th July 25,

2011 – This is being revised and rewritten]

The current system of issuing of refunds on excess

input-credits in VAT has led to numerous frauds. Inland Revenue of Sri Lanka, believing

limiting refunds, will reduce frauds introduced a voucher system to restrict the

number of refunds. Taxpayers as well as Inland Revenue officials feel the

voucher system a real nuisance and cumbersome to work. This may increase frauds

instead of reducing. Hence, A good system should not be too rigid to hamper

business activities but still possible to have some accountability. VAT-BILL,

an “I owe you” issued by the Inland Revenue can achieve this.

Standard System

A trader usually buys articles and sells them. When

he buys, pays VAT. When he sells, collects VAT. If the collected VAT is more

than what he paid he will have to remit the excess to Inland Revenue. If the collected

VAT is less than what he paid he will get a refund from the Inland Revenue.

Normal cross border transaction cycle

NOTE: -F refers to foreign and -L refers to local

·

Exporter-F

exports goods to Importer-L.

·

Exporter F

gets a refund from Government-F.

·

Importer-L

sells goods to Supplier-L and collects VAT.

·

Importer-L

pays VAT to Government-L.

·

Supplier-L

sells goods to Exporter-L and collects VAT.

·

Supplier-L

pays VAT to Government-L.

·

Exporter-L

exports goods to Importer-F

·

Exporter-L

gets a refund from Government-L.

·

Importer-F

pays VAT to Government-F.

The refunding is the most vulnerable function within the VAT system. Inland

Revenue has to rely upon the authenticity of the invoices submitted by the

trader. Two types of invoices can create fraudulent refunds. First, fake invoices — issued on bogus transactions — generate

refunds. Second, the invoices issued with regard to real

transactions, but the VAT portion is not remitted to Inland Revenue generate

refunds.

Inland Revenue employs various methods to stop giving fraudulent refunds

arising out of these invoices. VAT experts suggest to random check invoices and

give severe punishments to perpetrators. This method has several drawbacks. It is not a useful method because implementation of

the rule of law falls short in most countries.

Some countries including Sri Lanka utilize a

method to track the transactions by matching the vouchers. This seems very

difficult to implement. It consumes a large amount of resources, manpower and

computing. It tries to refuse the refund instead of punishing the wrongdoer –

this leads to further corruption. Real punishment is not blocking the fraud. It

will not deter the doer in repeating and others from not doing it.

Broad

outline of the proposed system

·

Issue of an

IOU—called V-bill— Instead of VAT a refund by the Inland Revenue is the first

step. The person who claimed Rs. 350,000 refund would receive three V-bills

with value Rs. 100,000 each—here the claim should be only Rs. 300,000 for the

current period and keep balance Rs. 50,000 to claim in the next period.

·

Dealing the V-bills

in the market by traders is the second step. They can trade these instead of

cash when they pay VAT on their purchases.

·

Redemption of the

V-bills by Inland Revenue accepting V-bills along with cash as VAT payments is

the last step.

A typical example to explain the system

Trader Sunil buys goods worth Rs. 5,000,000 — VAT Rs. 500,000 included

in it—from trader Kamala. Later, Sunil could only sell part of the goods worth Rs.

600,000 — he collects Rs. 60,000 as VAT. Sunil will get a refund of Rs. 440,000 at the end

of the tax period.

Instead of the refund Sunil will get four V-bills

each worth Rs. 100,000 — treatment of the balance Rs. 40,000 is explained

later. Sunil will transfer these V-bills together

with Rs. 4,600,000 to settle the debt he owes Kamala. In the end, Kamala will

surrender the V-bills in lieu of paying her VAT to Inland Revenue.

Cross Border transaction cycle

with local V-bill

NOTE: -F refers to foreign and -L

refers to local

·

Importer-L

will purchase goods from Exporter-F.

·

Exporter-F

will get a refund from Government-F.

·

Importer-L

will pay VAT/V-bills to Government-L.

·

Importer-L

will sell goods to Supplier-L and collect VAT/V-bills from him.

·

Supplier-L

will sell the goods to Exporter-L and collect VAT/V-bills from him.

·

Then

Supplier-L will pay the VAT/V-bills to Government-L.

·

Exporter-L

will export goods to Importer-F and collect V-bills from Government-L.

·

Importer-F

pays VAT to Government-F.

Issue of V-bills

· Taxpayer gets a refund in the form of V-bills when input

VAT is greater than output VAT.

· The refund claimer will have to produce the

necessary invoices for checking in order to obtain the refund.

·

This system

will stop issuing cheques as refunds arising from VAT input credit — some rare

refunds on erroneous returns and payments made by cash will be issued by

cheques.

·

Digital

V-bills can be issued by large taxpayers who can use it to reduce workload and

facilitate business to business transactions. These will have digital

signatures and have all the data usual paper V-bill has.

Denomination of V-bills

· Because of the sheer number of sales vouchers,

circulate in the market, cross matching them becomes difficult. By bundling a

set of vouchers into a single document (V-bill) that has a fixed denomination

will solve this. It will simplify the matching process. There will be only one

denomination (say Rs. 100,000). The system will process only these V-bills and

not the sales vouchers.

· The face value will be in only one denomination

preferably Rs. 100,000/- only.

· Trader can schedule the invoices so that the claim

is just above multiples of Rs. 100,000.

· In Sri Lanka VAT system issues refunds averaging to

Rs. 500m per month. Consequently around 5,000 V-bills will be issued per month.

The workload of Inland Revenue can be kept at reasonable limits by keeping

V-bill denomination to Rs. 100,000.

· If we have V-bills with multiple denominations, try

to capture data of each V-bill transfer, it will be too much data and will make

easy to hide any suspicious transactions. Too much of data will blur your

vision.

· When a taxpayer claims a VAT refund he will be

issued only VAT Bills to the nearest Rs. 100,000/- of the refund.

· V-bills can be used to make payment for purchases.

It will be allowed to make use V-bill to pay for the full value of the invoice

—it will not be limited to VAT value of invoice. V-bill value is for Rs.

100,000 which is fairly a high value. If this is allowed for VAT potion only it

will be difficult for small taxpayer to use it in their limited purchases. It

can be said that by allowing the V-bill to pay not only VAT but also the full

purchase value might lead to frauds. But system of V-bill will not be

operational and too cumbersome if the full value is not allowed.

· Taxpayers who do not have a refund

worth Rs. 100,000 in a single tax-period, can keep the

invoices without claiming until

the total refund is over Rs. 100,000. Then present it

for refund. One-year period will be given for them to use the invoices.

However, refunds will be rounded down to nearest Rs. 100,000 — If the

totals of the invoices are Rs. 115,000 he will get only one

Rs. 100,000 V-bill. Taxpayer will have to schedule their invoices and make

the claim to get the maximum benefit. They will be allowed one year to make the

claim on an invoice.

·

Split VAT Invoice: Legal provision has to be created to

issue two VAT invoices for a sale of a single item. This will allow the buyer

to claim one invoice in one tax period and the other invoice in another tax

period. This will help a buyer to round-up his input credit to nearest Rs.

100,000. By allowing this the buyer can get the full benefit of the input

credit while allowing Inland Revenue to manage their data in neat Rs. 100,000

units.

Maximum of only two split invoices could be used in

a refund claim for a taxable period. The responsibility of it should rest on

the buyer not the seller. A written request should be made by the buyer to the

seller. Each buyer can make only one such request to any of his sellers for a

taxable period —e.g. he cannot make two requests from two different sellers.

·

To overcome

the difficulty of exchanging the high denominated V-bill following concessions

regarding the time limit of dealing and redeeming are permitted:

◦

A trader can

keep the purchase invoices for one year before claiming credit.

◦

It will have a

validity period of preferably one year. It has to be redeemed with Inland

Revenue before that date.

◦

V-bill can be

transacted for a previous purchase done within the one year of the date of

V-bill— issue date.

Dealing

in V-bills

·

V-bill can be

traded legally with a seller for a purchase value more than 25% of the V-bill

value —Rs. 100,000 V-bill can be used to pay for a good of value Rs. 25,000 and

get balance in cash Rs. 75,000. This will reduce the disparities created by a

single high-value V-bill. If not the purchaser which makes multiple purchases

where each is less than the V-bill value, will be unable to redeem it. This

will effectively make possible to split the V-bill value by ¼ th and allow it

to be used against a lesser value than its fixed denomination.

·

Genuine

possessor of a V-bill will use it to pay for his purchasers and even settle his

debts on past purchasers.

◦

If money has

been paid regarding a purchase to the seller before the issue date of the

V-bill it can be transacted for money.

◦

If there is a

debt —unpaid invoice value— V-bill can be used to settle the debt.

· There will be no limit to the number of exchanges

of a V-bill from a seller to a purchaser. But only genuine purchases can

utilize it.

· Parties negotiating with V-bills will have to do it

on trust. It will be similar to cheques in Sri Lanka. We accept cheques only

from people we trust. This trust is the main safeguard against fraud to Inland

Revenue.

· It can be endorsed by parties negotiating with it

or any guarantors.

· It will have the qualities of a chose in action or

a nonnegotiable but transferable instrument — similar to a crossed cheque — an

IOU issued by the Inland Revenue.

·

V-bill will be

issued to a purchaser — VAT registered— only after the purchase, therefore, the

chance of using it to settle the debt —or VAT potion — arising from the same

purchase is little. By not limiting it to the VAT fraction, it can be used

in a future purchase. This will increase the chance of redeeming it.

Alternatively, the traders can agree to charge only the net value —without

VAT— from a sale and after the buyer gets his refund use the V-bill to

settle the VAT potion of the transaction.

·

Banks can

create a business of V-bill guarantying. They will endorse the V-bill for a

charge. They will check the business and vary the charge accordingly. It will

be an insurance against Inland Revenue rejecting the V-bill.

·

Credit-Rating

agencies can be created like CRIB to rate the vendors. This will help identify

a rate that should be applied in discounting the V-bills.

·

This will

create the concept of ‘careful trader’, who now assumed joint and several

liability for his actions and possibly those of others.

·

It will not be

compulsory for a trader to accept a V-bill; it is voluntary. He accepts it if

it helps him to do his trade. E.g. he may not be able to affect the sale if he

does not accept it. On the other hand, he has to be careful because of the

danger of incurring a loss by a rejected V-bill.

·

Inheritance in

case of ownership passing due to death, marriage, divorce, liquidation, etc.

And whether gifting should be allowed in limited circumstances should be

studied. Legal provision is necessary to allow the person inheriting it to make

an application to Inland Revenue to permit a transfer outside the scope of

normal transfer. This is an asset how to define its ownership may have to be

studied further. It has a limited life and scope to pass ownership. It has

limited method of redemption. If there is a breech at any point in the chain of

ownership, the value of it will become nil.

Enforcing of V-bills

· This will check data and other information to

detect possible fraud cases for investigation.

· In the event, V-bills that are issued but later found

to be incorrect Inland Revenue will issue assessments against the V-bill

presenter as well as it’s original owner.

·

When Inland

Revenue detects a breach of terms of a V-bill, it will, reject it, issue assessments disallowing it, transmit it

—In case of fraud, certificated copy will be given —to the taxpayer for damage

recovery purposes from other parties. Unless there is a breach of terms or a

fraud, the V-bill will remain valid not withstanding any issue of assessments.

·

If V-Bills can

legally be exchanged solely in lieu of purchases made, additional advantages

will creep into the V-bill system. The path of a V-bill from the time it is

issued at the time it is redeemed can be traced. A computer system will be able

to identify unusual paths —e.g. a V-bill issued to a textile exporter, redeemed

by a construction company appears uncommon. The limitation, V-bill holder can

deal it only with his suppliers curtails frauds.

·

Inland Revenue

will record at two points the transactions of each V-bill. To whom it is issued

and who redeems it.

·

It will be

possible to use Artificial Intelligence and fuzzy logic programs to identify

suspicious transactions. Inland Revenue needs good data to tackle fraud;

V-bills will supply it. Though minor random frauds may go, undetected,

large-scale frauds like the VAT fraud case will be indicated by the system. The

deviation in data patterns can be identified and suspicious V-bills can be

investigated.

·

Inland Revenue

will have to incur about Rs. 50,000 printing cost per month if V-bill needs to

have the security comparable to that of a cheque — a cheque leaf cost Rs. 10/-

·

2D or 3D bar

code can be incorporated to the V-bill leaf. It will be possible to insert

security data to these bar codes. In addition unique number with security can

be printed on it so that V-bills cannot be created by other than Inland

Revenue.

·

Inland Revenue

website will have a facility to check whether V-bill has already redeemed.

·

All presented

V-bills will be image scanned to keep a record of the persons who has endorsed

it.

·

It may be

necessary to create a separate Act by Parliament to deal in VAT Bills.

Liability Chain

·

Dealers in V-bills

have to obey by certain conditions. If these are violated Inland Revenue will

not allow credit to the presenter. If this happens, innocent third parties will

suffer losses. Then they can sue the other party for damages. Two types of

breaches can happen, technical breach and fraud breach. It first happens when conditions

stipulated for transfer is violated then damages can be claimed only up to the

point of violation by innocent parties. The second will occur when the taxpayer

fraudulently obtains the V-bill from Inland Revenue—he claimed a refund not due

to him. Here, damages can be claimed by innocent parties down the line.

·

The persons

buying the V-bill for cash and take possession of it and their guarantors will

be joint and severally liable for damages by innocent parties or assessment by

Inland Revenue on the value of the V-bill.

Fraud illustration: The

initial owner of a V-bill is A, and it will change hands to B, C, D, and E

respectively. E the final owner presents it to Inland Revenue claiming credit.

Later, Inland Revenue detects that A obtained this V-bill fraudulently. Inland

Revenue will issue two assessments one reversing the credit given on the V-bill

to E and the other reversing fraudulent refund made to A. Further to that A

will be prosecuted for fraud. B, C, D and E are innocent parties involved in

the chain of V-bill transaction. Here, each transferee can sue the transferor

—including guarantors — of the V-bill.

Breach illustration: A

breach occurs when the term of a V-bill is violated. The violation occurs in a

transfer in lieu of a purchase for a value less than Rs. 25,000. Suppose in a

transfer C will give the V-bill to D. D will give Rs. 80,000 —or may be less

because of the crooked transfer— and goods worth Rs. 20,000. While A, B and E

are innocent parties, both C and D are not. E will be assessed by Inland

Revenue because the V-bill presented by him is void. A and B there is no

liability. However, since E is an innocent party, he can sue D for damages.

Anti Fraud Enforcement

· Best way to combat VAT fraud is to make the VAT

refund go back the value addition chain in case of zero rated supplies.

· Advantage of the V-bill is that it will reduce

fraud but will not hinder the smooth operation of businesses like the current

VAT system.

· This will ensure government fund security. Even

when a fraud takes place, V-bills will stop VAT refunds siphoning out

government funds —famous VAT fraud. In case of fraud revenue from VAT will

reduce, but leakage of government funds will not occur.

Redeeming of V-bills

· It can be presented in lieu of VAT payments to

Inland Revenue —only VAT, not other taxes. Nevertheless, the original receiver

can use it to pay any tax administered by Inland Revenue.

· If V-bill is more than the VAT payable over payment

will be carried forward to be set off against a future date before V-bill

expires. Nevertheless V-bills will not be issued in place of redeemed V-bills.

· Inland Revenue will not allow any VAT credit on the

expired V-bills. To get value for a V-bill it must be presented before the due

date, failing that, it is not possible to set off even on behalf of VAT

charges that fall due before that date

· V-bills can be used to settle differed VAT at

Custom point. It will not be necessary to have a separate voucher system for

VAT differed at Customs. Taxpayers can use the same V-bills. With this

simplicity, it will make things easier for Inland Revenue and Customs.

Simplifying will also reduce fraud.

·

Inland Revenue

and Customs need to have procedures to handle redeeming of V-bills. Some

suggestions are:

o

Inland Revenue

will set up a counter similar to a shroff counter or bank counter where anyone

can submit V-bills with a voucher indicating the VAT number. This will be like

a counter where cash is accepted for tax payment.

o

It is possible

to outsource the above operation to a bank.

o

Similar

operation like in teller machines, V-bills will be inserted in a special sealed

envelope and indicate on the envelope the details of the taxpayer redeeming the

vouchers. A back-office operation will count V-bill s in the envelope and

record the necessary transactions.

What It will Do

·

Current system

in Sri Lanka

refuses the buyer his refund if the seller has not paid his VAT. A buyer pays

genuine cash (VAT included) to purchase some item. Then when he tries to claim

credit Inland Revenue will say, “look! The seller has not paid the VAT.

Therefore, we can’t pay your refund” In other words, there was a VAT fraud, we

— Inland Revenue— can’t bear the loss you have to bear it. These types of

arguments are outrageously inequitable because at the time of purchase the

buyer cannot know whether the seller will pay his VAT due in future — needs

divine knowledge, however, this is the current law.

·

With the

V-bill system, address this problem in a different way. The claimer will first

get his V-bill and will try to negotiate it with the seller for past or future

purchases. The fraudulent seller unwilling to declare his correct output tax

will be reluctant to get the V-bills since it will be of no use to him since he

is not paying any VAT and cannot utilize V-bills. If the buyer trade V-bills

with other parties for money it is illegal and there is a chance of getting

detected by the computer system since the transaction is an unusual one. This will

make the buyer reluctant to buy from that seller and will do business with

genuine ones. In the end, the seller will lose customers.

·

The seller

also will be cautious in dealing with other than money. The emphasis shifts

from a normal trading activity to a financial transaction. The set of rules

that apply will be different now. He will not like to deal in V-bills if he

doesn’t trust the purchaser is genuine. Inland Revenue may refuse to give

credit to the V-bill if the purchaser is legitimate. On the other hand, he

might lose his business if he doesn’t accept the V-bill. He will also have the

option of requesting the purchaser to ask someone whom the seller trusts to

guarantee the V-bill. Therefore, diverging forces will work and at some point

the business practices will get adjusted and have an equilibrium for the

benefit of both parties the taxpayer and Inland Revenue.

·

Still, the

seller can declare output only up to the value of V-bills and under declare the

balance sales. Nevertheless, even here there will be no revenue leakage due to

refunds. Furthermore, this type of activity may be flagged in the computer

system as suspicious.

·

If the public

can deal in V-bills like a typical bill of exchange, then, it will, turn into

an alternative currency, people can discount it through a bank, be an extremely

flexible instrument, it can be exchanged in lieu of money, be greatly

convenient to the taxpayers. Such a Bill will separate standard VAT, and VAT

created refunds. It will stop taxpayers siphoning non VAT government funds

through VAT system —VAT fraud. Even so, if such dealings are allowed V-bills

advantage will stop at that point because it will not stop reducing of VAT

revenue by claiming credit not due.

What it will not do

· V-bills will not stop altogether the frauds that

can be commuted making bogus invoices. However, making transferability of

V-bills limited only to genuine purchases by law will force the seller to

accept the V-bill on trust. Accepting V-bills from untrustworthy persons makes

the acceptor liable for assessments or damages. As a rule, it can be said these

frauds are committed with connivance. Usually several persons in the chain of

the transaction are involved in the fraud. Therefore, acceptors of the V-bills

will make sure that they accept only from genuine persons.

· It should be noted, V-bills will not stop bogus

claims altogether. Say a person buy something for his personal use and claim it

as input credit. V-bill system will not be effective in detecting these types

of fraud. But it will help identifying the main fraud in VAT, committed by

submitting bogus invoices to Inland Revenue to get refunds.

Problems Of Euro zone

·

Usually when

someone imports anything, VAT has to be paid at the Customs point. The importer

will be able to claim input credit for the VAT paid by him when he sells the

goods.

·

Inside Euro Zone,

VAT is not collected at the Customs point. Therefore, the importer when he

sells has to charge the VAT and pay it to the government.

·

Though Customs

do not collect VAT when goods cross the border, the exports are treated as zero

rated for VAT purposes and exporter will get a full refund of the VAT paid by him

in manufacturing the goods.

·

Therefore, if

the importer does not pay the VAT collected by him —missing trader— the revenue

loss is the whole VAT value, whereas if a normal trader does not pay VAT, the

revenue loss is only for the value addition done by him.

·

With V-bills

missing trader fraud will be limited only to the VAT slice since the missing

trader will have paid for his purchases or his imports through Customs —unlike Eurozone, Sri Lanka collects VAT at the

border.

·

Carousel

fraud will stop completely.

Because there is no cash refund. See http://en.wikipedia.org/wiki/Missing_trader_fraud

·

"Innocent

parties" - the 'Bond House' decision (http://en.wikipedia.org/wiki/Missing_trader_fraud#.22Innocent_parties.22_-_the_.27Bond_House.27_decision)

With V-bills innocent parties are protected. And Tax Authorities need not try

to minimize tax losses by disallowing input credit to innocent parties.

Future of VAT Bills

In

the future, the fixed denomination V-bills may change to variable bills. It may

be possible to operate an account like a bank account for the V-bills. Therefore,

purchasing using V-bills will be made easy.

Cross Border V-bills

Cross

border accepted V-bills will make V-bills go forward the supply chain. Usually

when it is dealt with the local supplier, it will go back the supply chain. In

future V-bills will be used to deal with the foreign importer allowing it to go

forward in the supply chain. The laws will have to change allowing V-bills to be

sold across borders.

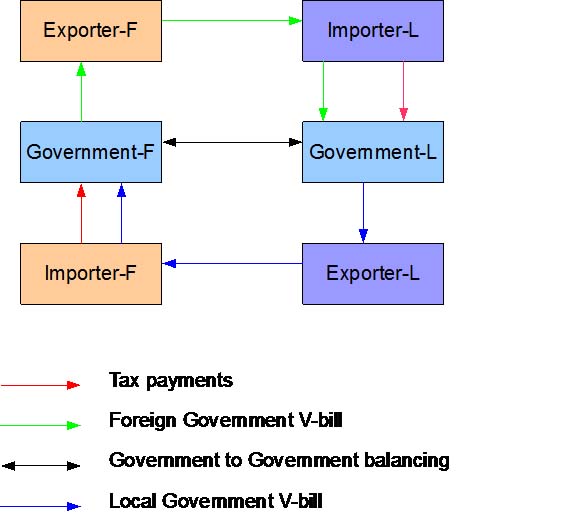

Cross Border with V-bill

NOTE:

-F refers to foreign and -L refers to local

·

The Extended

V-bill System can be applied by two or more willing governments by accepting

each other’s V-bills. This can reduce fraud (missing trader and carousal

frauds). Periodically, governments will balance the dues to each other. This is

similar to balancing Balance of Payments.

·

Suppose an Exporter-L

zero rated taxpayer — A VAT registered person that exports and does not

have to pay VAT to Inland Revenue, but his expenses will include VAT — and has

VAT paid invoices in his possession where he can claim input credit but is unable,

for some reason, to exchange it locally.

·

Exporter-L

sells goods to foreign Importer-F.

·

Then exporter-L

is allowed by law to sell these V-bills to Importer-F —may be a limit like 25%

of export value may be necessary for control purposes.

·

Importer-F can

use it to pay his VAT dues to his Government-F.

·

Later, Government-F

will balance with Government-L the V-bills.